CSRD: Danish rules on corporate sustainability reporting expected to apply to more enterprises than required by the EU

The long-anticipated Danish rules on corporate sustainability reporting are currently in public consultation until 24 November 2023. The public consultation is the first step in the Danish implementation of the Corporate Sustainability Reporting Directive (CSRD).

The rules are part of the EU’s comprehensive ESG regime, which aims to ensure enhanced transparency on the following issues:

- Environmental (climate and environment), e.g. companies’ impact on climate, including water, energy, carbon emission, circular economy.

- Social (social issues), e.g. respect for human rights, health and safety policies at the workplace, equal opportunities for all.

- Governance (corporate governance), e.g. transparency and disclosure in the reporting by a company’s management and the composition of the board of directors of a company.

The rules aim to ensure that capital and financing are channelled to economic activities that are sustainable. As a result, enterprises are to report on a variety of new matters.

The reporting is to be standardised through reporting standards called ESRS, which will ensure a higher degree of comparability in sustainability reporting.

Moreover, the level of information to be included in the reporting is regulated. This is based on the double materiality principle, which means that an enterprise must include information on the material impact of the enterprise on sustainability matters as well as information on how sustainability matters will affect the development, performance and position of the enterprise.

Danish implementation – Main points

- The Danish rules will apply to all large enterprises and all listed companies – which today include approx. 2,100 Danish enterprises. In addition to the enterprises falling within the scope of the CSRD, enterprises such as commercial foundations, cooperative societies and state-owned public limited companies will fall in scope. However, all these enterprises are at present already subject to requirements on a non-financial social responsibility report, cf. section 99 a of the Danish Financial Statements Act

- Apart from the scope, this is a minimum implementation, where the Danish rules will closely mirror the CSRD requirements. Denmark will also mirror the CSRD’s phased implementation for different enterprises to allow the enterprises time to adjust to the new requirements

- An auditor must provide a limited assurance sustainability statement on the contents of the sustainability reporting

- The management commentary must include a special section on sustainability. The non-financial information on sustainability is thus placed alongside financial information

- The double materiality principle is clarified

- A Danish priority will be to provide guidance to enterprises regarding sustainability reporting. A sum of DKK 40m has been allocated for this purpose

Change of thresholds

The draft rules will also introduce a change of the upper thresholds for micro, small and medium-sized enterprises. An enterprise is defined as small or medium-sized based on whether the enterprise exceeds any two of the following upper thresholds in two consecutive years:

Balance sheet total (DKK million)

Turnover (DKK million)

Number of employees

In practice, the raised thresholds will mean that many enterprises will move down one reporting class and that fewer enterprises will be required to report on sustainability.

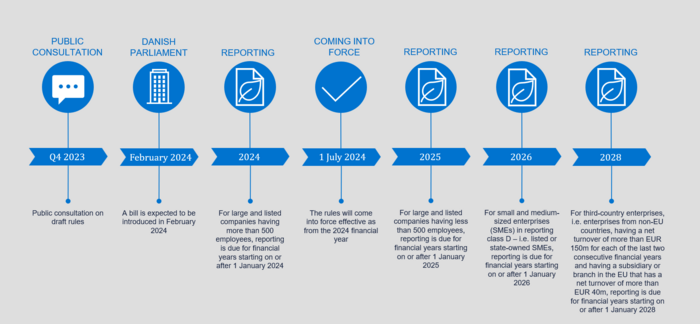

Implementation timeline

The implementation procedure will be as follows:

Not in scope?

Even if you do not fall directly within the scope of the CSRD implementation, we expect to see a strengthened focus generally on gathering and handling data from suppliers, business partners, etc. for in-scope enterprises. In-scope enterprises are required to include information on their entire value chains both within and outside the EU. Therefore, even small and medium-sized enterprises that do not fall within the scope of the rules may be expected to have to procure and deliver data on their own value chains to form part of the reporting by in-scope enterprises.

DLA Piper Denmark will monitor the sustainability reporting rules closely. DLA Piper Denmark’s specialists provide advice on all ESG aspects, including the scope and legal implications of the regulations, the adjustments to be made by enterprises in order to comply with the regulations, etc.