Sustainability reporting rules for insurance and reinsurance companies and multi-employer occupational pension funds in Denmark

On 22 May 2024, the Danish Parliament passed an important Act on sustainability reporting.

The title of the Act is Act no. 480 of 22 May 2024 on amendments to the Danish Financial Statements Act, the Auditors Act, and various other Acts (Implementation of the EU Directive on Corporate Sustainability Reporting and the EU Directive on raising the size thresholds in the Accounting Directive etc).

The Act implements the EU Corporate Sustainability Reporting Directive (CSRD) into Danish law, including in relation to insurance and reinsurance companies by amendments to the Insurance Business Act.

The new sustainability reporting rules in the amended Insurance Business Act came into force on 1 June 2024.

We provide comments on the new sustainability reporting rules for insurance and reinsurance companies. The rules are stated in the amended Insurance Business Act and the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds.

This newsletter contains the following sections:

- Main contents and scope of application of rules on sustainability reporting in Insurance Business Act and Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pensions Funds

- Insurance Business Act

- The making and scope of application of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

- Rules on sustainability reporting in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds as regards Danish undertakings

- The objectives of the Corporate Sustainability Reporting Directive (CSRD) and rules on sustainability reporting in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

- European Sustainability Reporting Standards (ESRS) and the rules of the Executive Order

- Specific rules on the content of the sustainability report under the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

- Auditor's report on the sustainability reporting

- Digital reporting and publishing of sustainability reporting

- Rules on sustainability reporting in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds as regards Danish subsidiary undertakings and branches of third-country undertakings

- Entry into force of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds and phased application of its rules on sustainability reporting in relation to different categories of undertakings from different dates of application

1. Main contents and scope of application of rules on sustainability reporting in Insurance Business Act and Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

The EU Corporate Sustainability Reporting Directive (CSRD) has been implemented into Danish law, including in relation to insurance and reinsurance companies and multi-employer occupational pension funds.

Covered undertakings must prepare and submit sustainability reporting in accordance with the rules stated in the directive.

The rules in the directive amend and insert new rules on sustainability reporting in the EU’s Directive 2013/34 on annual financial statements, consolidated financial statements and related reports of certain types of undertakings (as amended) (the Accounting Directive).

The rules on sustainability reporting in the Accounting Directive are stated in the following provisions, among others:

- Article 19a on sustainability reporting by undertakings.

- Article 29a on consolidated sustainability reporting by parent undertakings.

- Article 29b on sustainability reporting standards.

- Article 29c on sustainability reporting standards for small and medium-sized undertakings.

- Article 29d on a common electronic reporting format for sustainability reporting.

- Article 33, which obliges the members of the undertaking's administrative, management and supervisory bodies to ensure that the following documents are prepared and published in accordance with the directive’s requirements, including the sustainability reporting standards in articles 29b or 29c of the directive and the requirements for a common electronic reporting format in article 29d of the directive:

- The annual financial statements, management report, and the corporate governance statement, if presented separately.

- The consolidated financial statements, consolidated management reports, and the consolidated corporate governance statement, if presented separately.

- Article 34 on auditing and assurance of sustainability reporting.

The implementation in Danish law of the Corporate Sustainability Reporting Directive – and its amendments and insertions of new rules on sustainability reporting in the Accounting Directive – were made by Act no. 480 of 22 May 2024 on amendments to the Danish Financial Statements Act, the Auditors Act and various other Acts (Implementation of the EU Directive on Corporate Sustainability Reporting and the EU Directive on raising the size thresholds in the Accounting Directive etc.).

In relation to insurance and reinsurance companies and multi-employer occupational pension funds, the implementation mainly was made by adoption of provisions in Act no.718 of 13 June 2023 on Insurance Business (as amended) (the Insurance Business Act) and Executive Order no. 503 of 23 May 2024 on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds.

In this newsletter, insurance and reinsurance companies and multi-employer occupational pension funds are generally referred to as insurance companies.

The amended Insurance Business Act contains some main provisions on matters in relation to insurance companies' reporting of sustainability information in their annual reports in accordance with the EU Corporate Sustainability Reporting Directive (CSRD).

However, most of the provisions on these matters are stated in Executive Order no. 503 of 23 May 2024 on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds. The executive order was made under the amended Insurance Business Act.

As regards insurance and reinsurance companies and multi-employer occupational pension funds, the Directive is thus implemented into Danish law to some extent by the Insurance Business Act and to a much larger extent by the executive order.

In this newsletter, only the most important provisions of the act and the executive order are mentioned.

2. Insurance Business Act

In the Insurance Business Act, an insurance company is defined in section 9, subsection 1, item (1), as one of the following types of undertakings:

- A non-life insurance company.

- A mutual insurance company.

- A life insurance company.

- A multi-employer occupational pension fund.

- A reinsurance company.

In this newsletter, these insurance and reinsurance companies and multi-employer occupational pension funds are generally referred to as insurance companies.

An insurance company must for each financial year make an annual financial statement consisting of a balance sheet, an income statement, other comprehensive income, notes, including a statement on the accounting policies which are applied, and an overview of movements in equity. See section 178, subsection 1.

The annual financial statement must be supplemented with the following:

- A consolidated financial statement for a group led by the company.

- A management report for the company and for a group led by the company.

- A management endorsement.

- An auditor’s report.

See section 178, subsection 1.

If a statement on a sustainability report has been made in accordance with section 187 a, subsection 1, then it must be included in the annual report. See section 178, subsection 4.

Section 182, subsection 1, provides that once the annual report has been made, all members of the board of directors and the executive management must sign it and date the signature. The members must provide their signature in connection with a management statement, in which each member’s name and function in relation to the company is clearly indicated, and in which they declare different matters. Among other matters, they must declare whether the management report contains a true and fair account of the development in the company’s and, if a consolidated financial statement has been made, the group of companies’ activities and financial matters, as well as a description of the principal risks and uncertainties that may affect the company and the group. See section 182, subsection 1, nos. 1-3.

All members of the board of directors and the executive management must also declare that any sustainability reporting has been made in accordance with the rules thereon. See section 182, subsection 1, no. 3.

An undertaking which is required to make a sustainability report must ensure that the sustainability report is accompanied by a statement on sustainability reporting. The statement on sustainability reporting must be issued by an auditor who is authorised to issue statements on sustainability reporting under the rules thereon in the Auditor Act. See section 187a.

The sustainability reporting statement must be prepared and issued in accordance with the requirements set out in the EU's Corporate Sustainability Reporting Directive (CSRD). This directive includes rules which require an audit opinion on an undertaking’s sustainability reporting. The CSRD amends existing rules and introduces new rules on sustainability reporting in the EU’s Directive 2013/34 on annual financial statements, consolidated financial statements and related reports for certain types of undertakings (as amended), commonly known as the EU Accounting Directive. See the further comments below.

Under the amended and new rules in the Accounting Directive on corporate sustainability reporting, an auditor or independent assurance service provider must perform a limited assurance engagement on the sustainability information disclosed by the undertaking.

The auditor or assurance provider is required to issue an opinion based on a limited assurance engagement on the sustainability reporting. This opinion must confirm the sustainability reporting’s compliance with the Accounting Directive’s requirements. Additionally, the opinion must address the sustainability reporting's conformity with the sustainability reporting standards adopted pursuant to article 29b or 29c of the Accounting Directive. These are known as the European Sustainability Reporting Standards (ESRS). See article 29b of the Accounting Directive on general sustainability reporting standards and article 29c on specific sustainability reporting standards for small and medium-sized enterprises. See the further comments below.

The statement issued by the auditor or assurance service provider must also cover the process the undertaking has performed to identify the information reported under these sustainability reporting standards. Additionally, the statement must address the undertaking's compliance with the requirement to tag sustainability reporting in accordance with article 29d of the Accounting Directive. Furthermore, the statement must include comments on the undertaking’s compliance with the reporting requirements set out in article 8 of Regulation 2020/852 on the establishment of a framework to facilitate sustainable investments (the Taxonomy Regulation), as amended.

The requirements for the content of the statement also apply to any sustainability reporting for the undertaking’s group.

Accordingly, a covered undertaking must ensure that its sustainability reporting, or the group’s sustainability reporting, is accompanied by a sustainability reporting statement issued by an auditor or assurance service provider. This statement must be issued with limited assurance.

The specific requirements for the content of an auditor's statement on sustainability reporting are set under the Auditors Act in Executive Order no. 518 of 24 May 2024 on statements by approved auditors.

Based on article 29b of the Accounting Directive, general European standards for sustainability reporting (European Sustainability Reporting Standards (ESRS)) have been established by Commission Delegated Regulation 2023/2772, which provides supplementary rules to the Accounting Directive 2013/34 regarding sustainability reporting standards.

Under article 29c of the Accounting Directive, the Commission may establish specific European sustainability reporting standards for small and medium-sized enterprises (SMEs). As of November 2024, the Commission is in the process of developing these standards. A draft of these specific standards was open for consultation in spring 2024, and the final specific standards are expected to be adopted in early 2025. The purpose of these specific standards is to reduce the reporting burden on SMEs by providing to them the option to apply simplified specific sustainability reporting standards tailored to their more limited resources and needs, should they prefer these over the more comprehensive general standards. Until the final specific standards are adopted, SMEs are not required to apply any particular sustainability reporting standards. However, they may voluntarily choose to apply the general sustainability reporting standards in the interim.

An undertaking which is required to make a sustainability report, and which under other legislation must have parts of its sustainability report verified by an accredited independent third party, must make the report from the independent third party available on the company's website. See section 189, subsection 3.

3. The making and scope of application of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

The Financial Supervisory Authority sets rules for sustainability reporting, including rules on content and form. See section 190, subsection 4.

The Financial Supervisory Authority has used the authority under section 190, subsection 4, of the Insurance Business Act to issue Executive Order no. 503 of 23 May 2024 on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds.

In the executive order, section 1, subsection 1, provides that the executive order applies to the following undertakings:

- Insurance companies.

- Pension funds comprised by the Insurance Business Act (multi-employer occupational pension funds).

- Insurance holding undertakings and financial holding undertakings whose business consists exclusively or primarily of holding equity interests in insurance companies.

Under section 9, subsection 1, item (1), of the Insurance Business Act, the term insurance company also comprises a reinsurance company. This also applies in relation to the executive orders and its section 1, subsection 1, on its scope of application.

The executive order thus applies to all these types of insurance and reinsurance companies, multi-employer occupational pension funds, insurance holding undertakings and financial holding undertakings whose business consists exclusively or primarily of holding equity interests in insurance companies.

The provisions on sustainability reporting in the executive order generally apply to all these companies, funds and undertakings, subject to the more specific provisions on the scopes and times of application of the provisions on sustainability reporting.

4. Rules on sustainability reporting in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds as regards Danish undertakings

Certain undertakings must make a sustainability report and include it in their management report in the annual report.

The undertakings which have sustainability reporting obligations are:

- Large undertakings.

- Small and medium-sized undertakings which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA).

See section 144a in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds.

See the comments below on these types of undertakings.

Small and medium-sized undertakings which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA) and captive insurance undertakings and captive reinsurance undertakings may limit their sustainability reporting in accordance with the sustainability reporting standards for small and medium-sized undertakings, as established by the EU Commission. The EU Commission establishes these standards through delegated acts under article 29c of the EU Directive 2013/34 on annual financial statements, consolidated financial statements and related reports of certain types of undertakings (the Accounting Directive). See section 144b in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds.

Section 144b applies to small and medium-sized undertakings which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA), large captive insurance undertakings and captive reinsurance undertakings, and small and medium-sized captive insurance undertakings and captive reinsurance undertakings which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA).

Section 144a provides which information shall be included in the sustainability report. The reporting must include information necessary to understand the undertaking's impacts on sustainability matters and how sustainability matters affect the undertaking's development, performance and situation. This includes a description of the undertaking’s business model and business strategy, sustainability goals, roles of the management, the undertaking’s policies regarding sustainability matters, the undertaking’s sustainability due diligence procedures and many other sustainability reporting matters.

Section 144a contains many and comprehensive provisions on the covered undertakings' sustainability reporting obligations and related matters. The provisions are based on and implement the provisions of the EU Corporate Sustainability Reporting Directive (CSRD).

5. The objectives of the Corporate Sustainability Reporting Directive (CSRD) and rules on sustainability reporting in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

The purpose of the EU Sustainability Reporting Directive (CSRD) generally is to promote, improve and increase corporate sustainability reporting.

It aims to promote and support the work of EU companies in achieving the goals of the European Green Deal and the UN Sustainable Development Goals.

The Corporate Sustainability Reporting Directive also supports the work on sustainable financing among companies and their investors and lenders, including financial institutions. This is supported by ensuring that investors and lenders have access to relevant, comparable and credible information on sustainability.

Sustainability reporting regulations include detailed requirements for companies to report on sustainability matters. These are often referred to as Environmental, Social and Governance (ESG) matters. They include environmental and climate ("E") matters, human rights, labour and other social ("S") matters and corporate governance ("G") matters.

Covered companies must now disclose significantly more comprehensive and standardised information on a range of sustainability matters compared to the requirements previously imposed on companies under the Non-Financial Reporting Directive.

A covered company's auditor must now issue a limited assurance opinion on the sustainability reporting. Under the previous rules, an auditor only had to provide an opinion based on a so-called consistency check.

The purpose of the Executive Order is generally the same as the purpose of the Corporate Sustainability Reporting Directive. The purpose of the Executive Order is also to establish and strengthen the framework for undertakings' sustainability reporting in the management commentary in the annual report.

Undertakings' work on sustainability reporting is considered central to their work on sustainability and the green transition. It is important that sustainability reporting is both credible and usable for financial users.

The recitals in the preamble of the Corporate Sustainability Reporting Directive mention two main groups of users.

The first group of users is investors, including asset managers. They want to gain a better understanding of the risks and opportunities associated with sustainability matters for their investments. They also want to better understand the impact of their investments on people and the environment.

The second group of users is civil society actors, including non-governmental organisations (NGOs) and social partners (labour market parties), among others. They want to make companies take more responsibility for the impact of their activities on people and the environment. Many other stakeholders can also make use of the information. For example, to assess and compare companies and their sustainability performance and activities, including within sectors and across sectors.

For funding and investment to be targeted towards truly sustainable businesses and projects, it is necessary that sustainable companies can be identified based on specific data. Capital and demand can then be directed towards these companies.

Standardised sustainability data also allows for better comparability of companies' sustainability performance and activities, including within sectors and across sectors.

Sustainability reporting also gives some companies a competitive advantage if they do it earlier, better and on a larger scale than their competitors.

The aim of the Executive Order is also to enable investors, civil society organisations and other stakeholders to better assess the sustainability of undertakings through sustainability reporting. They can then better channel funding and demand towards the most sustainable undertakings. On the other hand, undertakings that are not sustainable or do not show it in their reporting can be challenged in terms of access to financing and demand for their products.

6. European Sustainability Reporting Standards (ESRS) and the rules of the Executive Order

Reporting must be done in accordance with the applicable European standards. They are called the European Sustainability Reporting Standards (ESRS).

The EU Corporate Sustainability Reporting Directive (CSRD) requires standards to specify the information which companies must disclose in their sustainability reports. This includes information on environmental matters, including climate, water and marine resources, resource use, circular economy, pollution, biodiversity and ecosystems ("E"). It also includes information on social matters, human rights and labour rights matters ("S") and corporate governance matters ("G").

The sustainability reporting standards are directly applicable in the Member States and do not need to be implemented into Danish law. The rules of the Corporate Sustainability Reporting Directive (CSRD) set the framework for the application of the sustainability reporting standards.

The framework for sustainability reporting regarding insurance companies has been implemented into Danish law by the making and issuance of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds. The Executive Order contains provisions on sustainability reporting. The framework for sustainability reporting is thus provided in the Executive Order.

According to section 144a, subsection 7, of the Executive Order, a covered undertaking must make a sustainability report in accordance with the sustainability reporting standards which are applicable from time to time under European law.

The Corporate Sustainability Reporting Directive clarifies the double materiality principle by establishing rules for a double materiality assessment.

Covered undertakings must apply a double materiality assessment when preparing their sustainability reporting. An undertaking must use the double materiality assessment to assess and understand the undertaking's impact on sustainability matters and to assess and understand how sustainability matters affect the undertaking's development, performance and position. The outcome of the undertaking's double materiality assessment determines the disclosure requirements and the information that the undertaking must include in its sustainability reporting.

According to section 144a of the Executive Order, a covered undertaking must include the sustainability report in the management commentary in the annual report. The reporting must constitute a separate section in the management commentary.

The reporting must include information necessary to understand the undertaking's impact on sustainability matters and how sustainability matters affect the company's development, performance and position.

The undertaking must disclose the process it has undertaken to identify the information included in the reporting.

7. Specific rules on the content of the sustainability report under the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds

According to section 144a, subsection 3, of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds, a covered undertaking's sustainability reporting must include a number of specified information. In particular, it is information on the following matters.

The undertaking’s business model and strategy in relation to sustainability matters

The sustainability reporting must include a brief description of the undertaking’s business model and strategy, including in relation to the following sustainability matters:

(a) The resilience of the undertaking’s business model and strategy to risks related to sustainability matters.

(b) The undertaking’s capabilities regarding sustainability matters.

(c) The undertaking’s plans, including implementation actions and related financing and investment plans, to ensure that its business model and strategy are consistent with the Paris Agreement under the United Nations Framework Convention on Climate Change (2015) and with the objective of achieving climate neutrality by 2050 as set out in the EU Regulation establishing a framework to achieve climate neutrality. Where applicable, the company must also disclose its exposure to coal, oil and gas related activities.

(d) How the undertaking’s business model and strategy take into account the interests of its stakeholders and its impact on sustainability matters.

(e) How the undertaking’s strategy has been implemented with regard to sustainability matters.

The undertaking’s time-bound sustainability targets

The sustainability reporting must include a description of the undertaking’s established time-bound sustainability targets.

Where applicable, the reference shall include absolute greenhouse gas emission reduction targets for at least 2030 and 2050.

The reporting shall also include a description of the undertaking’s progress towards achieving these targets and an indication of whether the undertaking’s targets regarding environmental factors are based on scientific evidence.

The role and expertise of the undertaking’s management in relation to sustainability

The sustainability reporting must include a description of the role the undertaking’s management plays with regard to sustainability matters.

The reporting must also include a description of the management's expertise and skills to fulfil this role or the ability of management to use assistance in relation to this.

Company policies and any incentive schemes related to sustainability matters

The reporting must include a description of the undertaking’s policies regarding sustainability matters.

The reporting must also state whether there are incentive schemes related to sustainability matters offered to members of the undertaking’s management.

Due diligence procedures, significant actual or potential adverse impacts and measures to prevent, mitigate, remedy or stop actual or potential adverse impacts

The reporting must include a description of the undertaking’s matters and activities in relation to the following sustainability factors:

(a) Due diligence procedures carried out by the company with regard to sustainability matters. Where applicable, this must be in accordance with other legislation requiring undertakings to conduct a due diligence procedure. For very large undertakings, this will include the EU directive on corporate sustainability due diligence. It is called the Corporate Sustainability Due Diligence Directive (CSDDD).

(b) The main actual or potential negative impacts relating to the undertaking’s own activities and its value chain. Its value chain includes its products and services, its business relationships and its supply chain. The reporting must also address the undertaking’s actions to identify and monitor these impacts and other negative impacts which the company is required to identify under other legislation on due diligence by undertakings. For very large undertakings, this will include the EU Corporate Sustainability Due Diligence Directive (CSDDD).

(c) Any actions taken by the company to prevent, mitigate, remedy or halt actual or potential adverse impacts and the outcome of such actions.

The undertaking’s main risks related to sustainability matters

The sustainability reporting must include a description of the most significant risks for the company regarding sustainability matters.

The reporting must include a description of the undertaking’s key dependencies in relation to these matters and how the company manages these risks.

Indicators, time horizons and the company value chain

The sustainability reporting must include information on indicators that are relevant to the other information mentioned above in the reporting.

The reporting of the above information shall include information regarding short-term, medium-term and long-term time horizons, as appropriate.

The above-mentioned information in the reporting shall include, where applicable, the undertaking’s own activities and its value chain, including its products and services, its business relationships and its supply chain.

8. Auditor's report on the sustainability reporting

According to section 187a of the Insurance Business Act, an undertaking which is required to make a sustainability report must include a statement from an auditor on the sustainability reporting.

The statement may only be issued by an auditor authorised to issue sustainability reporting statements under the Danish Auditors Act.

According to section 16, subsection 5, of the Danish Auditors Act, the Danish Business Authority may set rules and standards on ethics, the organisation and performance of audit services and the auditor’s issuance of audit reports, including auditor’s statements on the management reports etc.

The Danish Business Authority has used this authorisation to set rules in the Executive Order no. 518 of 24 May 2024 on Authorised Auditors’ Statements.

Section 17 of the Executive Order on Authorised Auditors’ Statements provides that a statement from an auditor on the sustainability reporting shall, as a minimum, include the following:

(a) An identification of the sustainability reporting which is being audited. The identification shall state the undertaking whose sustainability reporting is the subject of the statement, the balance sheet date, the period covered by the sustainability reporting and the reporting conceptual framework which is used in the drafting of the sustainability reporting.

(b) A description of the auditor’s responsibilities and performed work. The description of the performed work must include a description of the purpose and nature of the statement, including information on the standards applied in the statement. When the European Commission has adopted a standard for statements engagements on sustainability reporting, such standard must be followed.

(c) Modifications, if applicable. The auditor must modify the conclusion if the information used as a basis for the performed work is insufficient or incorrect, or if the auditor is unable to obtain sufficient and appropriate documentation that the subject matter is free from errors. In addition, the auditor must modify the conclusion if any uncertainties are not disclosed in an adequate manner or if any uncertainties are essential.

(d) A conclusion regarding the performed work. The conclusion must have the title “Conclusion”. The conclusion must be provided with limited assurance, as a minimum. This is to ensure the credibility of the sustainability information and thus the fulfilment of the needs of the intended users of the information. The conclusion may also be provided with high level of assurance. The auditor’s conclusion must state, among other matters, whether the auditor has become aware of matters which cause the auditor to conclude that the sustainability reporting has not been made in accordance with the applicable rules and regulations or in accordance with the process performed by the company to identify the information to be included in the sustainability reporting under the sustainability reporting standards.

(e) Emphasis of matters, if applicable. The auditor must provide information on any matter which the auditor highlights without modifying the conclusion. Any such information may not replace a modification to the conclusion, as stated above in item (c).

9. Digital reporting and publishing of sustainability reporting

Articles 19a and 29a of the Corporate Sustainability Reporting Directive require an undertaking's sustainability information to be clearly identified in a separate section of the management commentary in the annual report.

The same requirement follows from the amended rules in the Insurance Business Act on sustainability reporting.

Section 189, subsection 4, of the Insurance Business Act provides that the Financial Supervisory Authority may, after negotiation with the Danish Business Authority, set rules on the submission of annual reports and interim reports to the Danish Business Authority and rules on the publication of annual reports and interim reports.

The Financial Supervisory Authority has used this authority to set rules thereon in the Executive Order no. 736 of 14 June 2024 on Reporting to and Publication of Annual Reports etc in the Danish Business Authority for Undertakings covered by Accounting Rules under or pursuant to Legislation for Financial Undertakings etc.

Section 3, subsection 3, of the Executive Order provides that undertakings which make sustainability reporting must make and report the undertaking’s annual report in accordance with section 3, subsections 5 and 6. Moreover, when labelling the annual report, the undertaking must apply both the taxonomy specified by the Financial Supervisory Authority and the ESRS taxonomies which are in force from time to time, as published by the European Securities and Markets Authority (ESMA).

Under section 3, subsection 5, undertakings which do sustainability reporting must make their annual reports by using the relevant taxonomies, as specified by the Financial Supervisory Authority. The taxonomy is published on the Financial Supervisory Authority’s website at any time.

Under section 3, subsection 6, the annual report must be submitted to the Danish Business Authority by using a digital reporting solution called “Regnskab Special” which may be accessed through the Danish Business Authority’s website. An undertaking’s sustainability report must thus be submitted digitally to the Danish Business Authority as part of the undertaking’s annual report, which must be submitted digitally.

Section 3, subsection 8, provides that the Danish Business Authority publishes the annual reports to ensure that accounting users have access to accounting documents at any time through the Danish Business Authority’s website.

Section 5 provides, among other matters, that an annual report must contain an auditor’s statement on sustainability reporting if the undertaking makes sustainability reporting. It also provides that the undertaking must keep a copy of the accounting document, which is signed by the auditor, if the accounting document has been subject to audit or reviewed, and a copy of the accounting document which is signed by the auditor who has issued a statement on sustainability reporting, if the accounting document contains a sustainability report.

10. Rules on sustainability reporting in the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds as regards Danish subsidiary undertakings and branches of third-country undertakings

Sections 170-172 of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds contain provisions on sustainability reports to be made by certain Danish subsidiary undertakings and branches of third-country undertakings on behalf of the third-country undertakings as regard the Danish subsidiary undertakings and branches.

Sections 170, subsection 1, applies to such a Danish subsidiary undertaking covered by section 144 a, which is part of a group of undertakings whose total gross premiums in the EU exceed EUR 150 million in each of the last two consecutive financial years, and which has an ultimate parent undertaking which is not subject to the legislation of a member state of the EU or the European Economic Area (EEA). Sections 170, subsection 1, provides that such a Danish subsidiary undertaking must, on behalf of the ultimate parent undertaking, make and submit a sustainability report in accordance with the requirements for the content of the sustainability report in section 172 and publication in section 189a of the Insurance Business Act. The subsidiary undertaking must also have the sustainability report accompanied by a sustainability reporting statement as provided in section 189a of the Insurance Business Act. However, these requirements do not apply if the ultimate parent undertaking has made and submitted a sustainability report at the group level which meets the requirements of section 172 in the executive order. Sections 170, subsections 2-6, of the executive order contain further provisions on the sustainability reporting obligations of the subsidiary undertaking and the ultimate parent undertaking.

Sections 171, subsection 1, applies to a Danish branch whose gross premiums in the previous financial year exceeded EUR 40 million, and which is a branch of an undertaking which is not subject to the legislation of a member state of the EU or the European Economic Area (EEA), if (1) the foreign undertaking is not part of a group, and the undertaking's gross premiums in the EU exceeded EUR 150 million in each of the last two consecutive financial years, or (2) the foreign undertaking is part of a group of undertakings whose ultimate parent undertaking is not subject to the legislation of a member state of the EU or the European Economic Area (EEA), and the group’s total gross premiums in the EU exceeded EUR 150 million in each of the last two consecutive financial years. Sections 171, subsection 1, provides that such a Danish branch must, on behalf of the third-country undertaking, make and submit a sustainability report in accordance with the requirements for the content of the sustainability report in section 172 and publication in section 189a of the Insurance Business Act, either regarding the foreign undertaking if it is not part of a group of undertaking or regarding the entire group if it is part of a group of undertaking. The branch must also have the sustainability report accompanied by a sustainability reporting statement as provided in section 189a of the Insurance Business Act. Sections 171, subsection 2, of the executive order provides that subsection 1 does not apply (1) if one of the third-country undertakings mentioned in subsection 1, no. (1) or (2), has made and submitted a sustainability report which meets the requirements in section 172 of the executive order, or (2) if one of the said third-country undertakings has a subsidiary undertaking comprised by section 144a as provided in section 170 of the executive order. Sections 171, subsections 3-7, contain further provisions on the sustainability reporting obligations of the branch and the third-country undertakings mentioned in subsection 1, no. (1) or (2).

Sections 172 contains further provisions on the sustainability reporting obligations of the Danish subsidiary undertakings, the Danish branches and the third-country undertakings which must make and submit sustainability reports under sections 170 and 171.

11. Entry into force of the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds and phased application of its rules on sustainability reporting in relation to different categories of undertakings from different dates of application

It follows from section 174, subsection 1, that the Executive Order on Financial Reports for Insurance Companies and Multi-Employer Occupational Pension Funds entered into force on 1 June 2024.

Section 174, subsections 2-8, provide that the rules on sustainability reporting in sections 144a and 144b apply to different types of undertakings from different dates, in accordance with a phased application as also provided in the EU Corporate Sustainability Reporting Directive (CSRD).

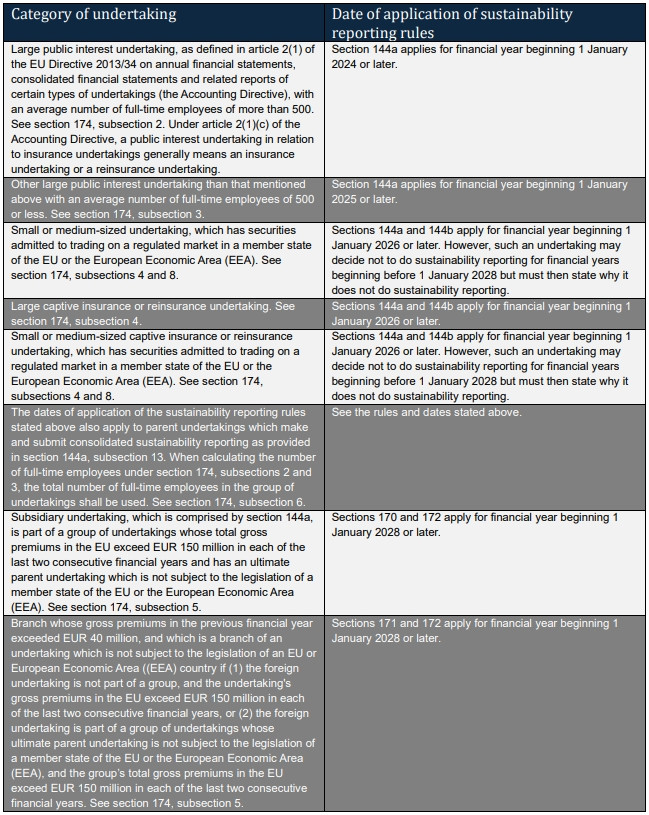

Section 174, subsection 2, provides that section 144a applies for financial years beginning on 1 January 2024 or later for large public interest undertakings, as defined in article 2(1) of the EU Directive 2013/34 on annual financial statements, consolidated financial statements and related reports of certain types of undertakings (the Accounting Directive), which had an average number of full-time employees of more than 500 during the financial year at the balance sheet date. The public interest undertakings are generally insurance companies and reinsurance companies as defined in the Insurance Business Act. See the comments below on the definition of large undertakings in annex 1 to the executive order.

Section 174, subsection 3, provides that section 144a applies for financial years beginning on 1 January 2025 or later to large undertaking not covered by subsection 2. These undertakings are generally large undertaking which had an average number of full-time employees of 500 or less during the financial year at the balance sheet date.

Section 174, subsection 4, provides that sections 144a and 144b apply for financial years beginning on 1 January 2026 or later to (1) small and medium-sized undertakings, which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA), (2) large captive insurance and reinsurance undertakings, and (3) small and medium-sized captive insurance and reinsurance undertakings, which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA). See the comments below on the definition of small, medium-sized and large undertakings in annex 1 to the executive order.

Section 174, subsection 5, provides that sections 170-172 apply for financial years beginning on 1 January 2028 or later. Sections 170-172 contain provision on sustainability reports to be made by certain EU subsidiary undertakings and branches of third-country undertakings on behalf of the third-country undertakings as regard the EU subsidiary undertakings and branches. See the comments above.

Section 174, subsection 6, provides that subsections 2-4 also apply to parent undertakings which make and submit consolidated sustainability reporting as provided in section 144a, subsection 13. When calculating the number of full-time employees under subsections 2-3, the total number of full-time employees in the group of undertakings shall be used.

Section 174, subsection 8, provides that small and medium-sized undertakings which have securities admitted to trading on a regulated market in a member state of the EU or the European Economic Area (EEA) may, notwithstanding section 144a, subsection 2, decide not to include sustainability reporting in the management report for financial years beginning before 1 January 1 2028, but must in such cases state why the reporting is not included in the management report.

The following table shows the phased application of sections 144a and 144b to different types of undertakings from different dates:

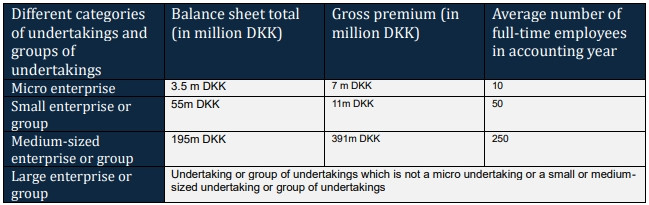

The provisions in section 174 on the phased application of sections 144a and 144b to different types of undertakings from different dates are based on the definitions of different types of undertakings in annex 1 to the executive order.

The following table shows the definitions of different categories of undertaking and groups in annex 1, item 13. Figures are in million Danish kroner (DKK) for the financial year. Under the definitions of different categories of undertakings and groups, the definitions of different categories of undertakings apply correspondingly to the definitions of different categories of groups of undertakings. Under the definitions of different categories of undertakings and groups, an undertaking or a group of undertakings is comprised by a definition if the undertaking or the group for two consecutive financial years at the balance sheet date does not exceed the numerical limits for at least two of the following three criteria:

- Insurance and Liability Disputes

- Global Employment Law Compliance

- Employee and Labor Relations

- Pensions and Reward

- Global Governance and Compliance

- Diversity, Discrimination and Equal Pay

- Workforce Restructuring and Outsourcing

- Regulatory issues in the financial sector

- International trade, investment, regulation and compliance

- Capital Markets and Listed Companies

- Corporate law and Corporate Governance